Key points

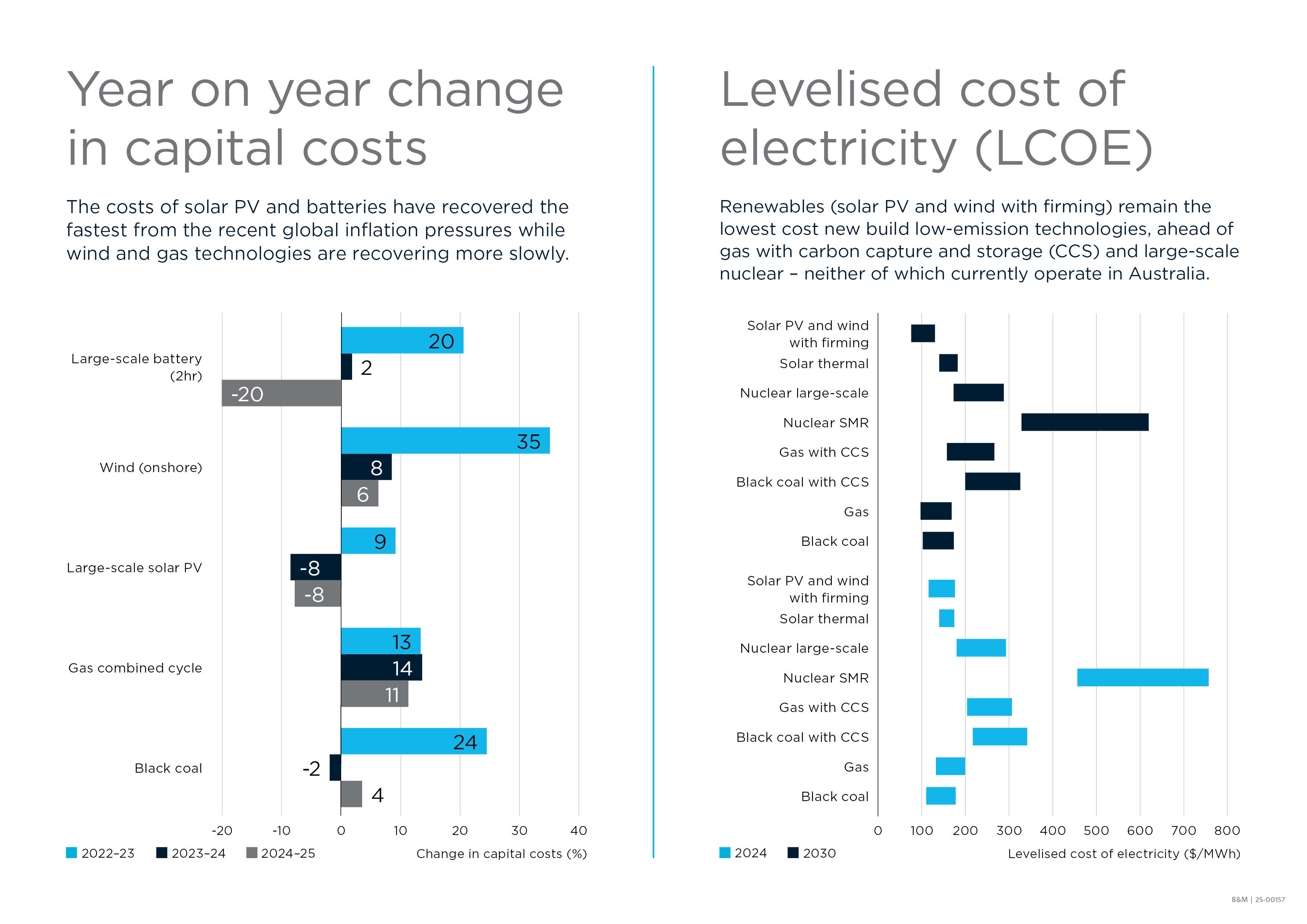

- The report found renewables remain the lowest-cost new-build electricity generation technology, while nuclear small modular reactors (SMRs) are the most costly.

- Electricity systems rely on a mix of technologies, because no single option can deliver all the capabilities required for a reliable, secure and flexible supply.

- Rising construction costs in Australia and supply chain constraints for some technologies remain a challenge for reducing costs.

CSIRO, Australia’s national science agency, today released the final 2024-25 GenCost Report in collaboration with the Australian Energy Market Operator (AEMO).

The GenCost report provides cost data for a range of new-build electricity generation technologies to support electricity system modelling and planning.

While some technologies are more cost-effective than others, a mix of technologies will be required to ensure system reliability and flexibility over the long term.

The report found renewables (wind and solar) backed by storage and transmission remained the lowest-cost new-build electricity generation technologies.

Gas with carbon capture and storage (CCS) and large-scale nuclear are the next lowest cost options, but as neither are currently deployed for electricity generation in Australia, they could be subject to longer lead times and first-of-a-kind premiums.

Small modular nuclear reactors (SMRs) remain the highest cost option, even with new data from Canada’s Darlington project. This represented the first commercial-scale benchmark from a western country and fell within the range previously projected by GenCost.

CSIRO’s Director of Energy, Dr Dietmar Tourbier, said GenCost is Australia’s most comprehensive source of electricity generation cost projections, supporting evidence-based decisions across the sector.

“GenCost delivers transparent, independent cost estimates that feed directly into electricity system modelling and investment planning,” Dr Tourbier said.

“We refresh forecasts annually using the best available data at the time to ensure GenCost reflects current market conditions and remains a trusted benchmark.”

“By drawing on expert input from across the electricity sector, GenCost reinforces CSIRO’s role as a neutral source of scientific insight to help guide Australia’s energy transition,” he said.

CSIRO’s Chief Energy Economist and GenCost lead author, Mr Paul Graham said fewer submissions were received in the stakeholder consultation process than in previous cycles, but reflected a broader range of perspectives.

“Most input we received focused on technologies already in development or under construction, such as pumped hydro, wind, solar photovoltaics (PV), gas, solar thermal and electrolysers,” Mr Graham said.

“The strength of GenCost lies in collaboration. We depend on the deep expertise of the electricity industry because no single organisation can track every technology in detail.”

Following consultation, cost projections for most technologies have been revised upwards, despite continued declines in solar PV and battery costs. Key drivers of these changes include:

- New data indicating sustained long-term increases in Australian construction costs

- Inclusion of work camp costs in capital estimates for future wind projects

- Market intelligence suggesting global gas turbine supply may lag demand in coming years

- An increase in capital financing rates to align with assumptions in other major studies.

AEMO Executive General Manager System Design, Merryn York, said GenCost is one of several key reports that help support Australia’s energy system planning.

“AEMO supports the CSIRO, as the author of the GenCost report, by commissioning current generator capital cost estimates,” Ms York said.

“We’ll use the capital costs for generation and storage from GenCost in the upcoming Draft Integrated System Plan in December,” she said.

Access the GenCost 2024-25 Final Report and background resources.

Learn more about CSIRO's energy research.

{kind=link}